The landscape of long-term care (LTC) in the U.S. is at a critical juncture. With an aging American demographic—all Baby Boomers will be 65+ by 2030, swelling the elder population to over 70 million—the demand for LTC services is surging. Currently, over 12 million Americans require LTC, and the costs are staggering, with nursing homes averaging over $100,000 annually. This escalating need, coupled with the complexities of existing insurance models and the high premiums of LTC insurance, highlights an urgent call for transformation.

Historically, LTC was largely family-supported. The advent of Medicare and Medicaid in 1965 addressed acute care and low-income needs respectively, but left a significant gap for custodial care—assistance with daily activities like bathing and dressing, without direct medical intervention.1 This gap is precisely what LTC insurance was designed to fill. However, its market penetration remains low due to high costs, complex policies, and a general lack of consumer understanding.

Key factors driving high LTC premiums include:

The long duration and uncertainty of potential claims.

Inflation risk in care costs.2

Complex underwriting and claims processing.3

Increasing longevity and chronic illness prevalence, particularly cognitive impairments like dementia and Alzheimer's.

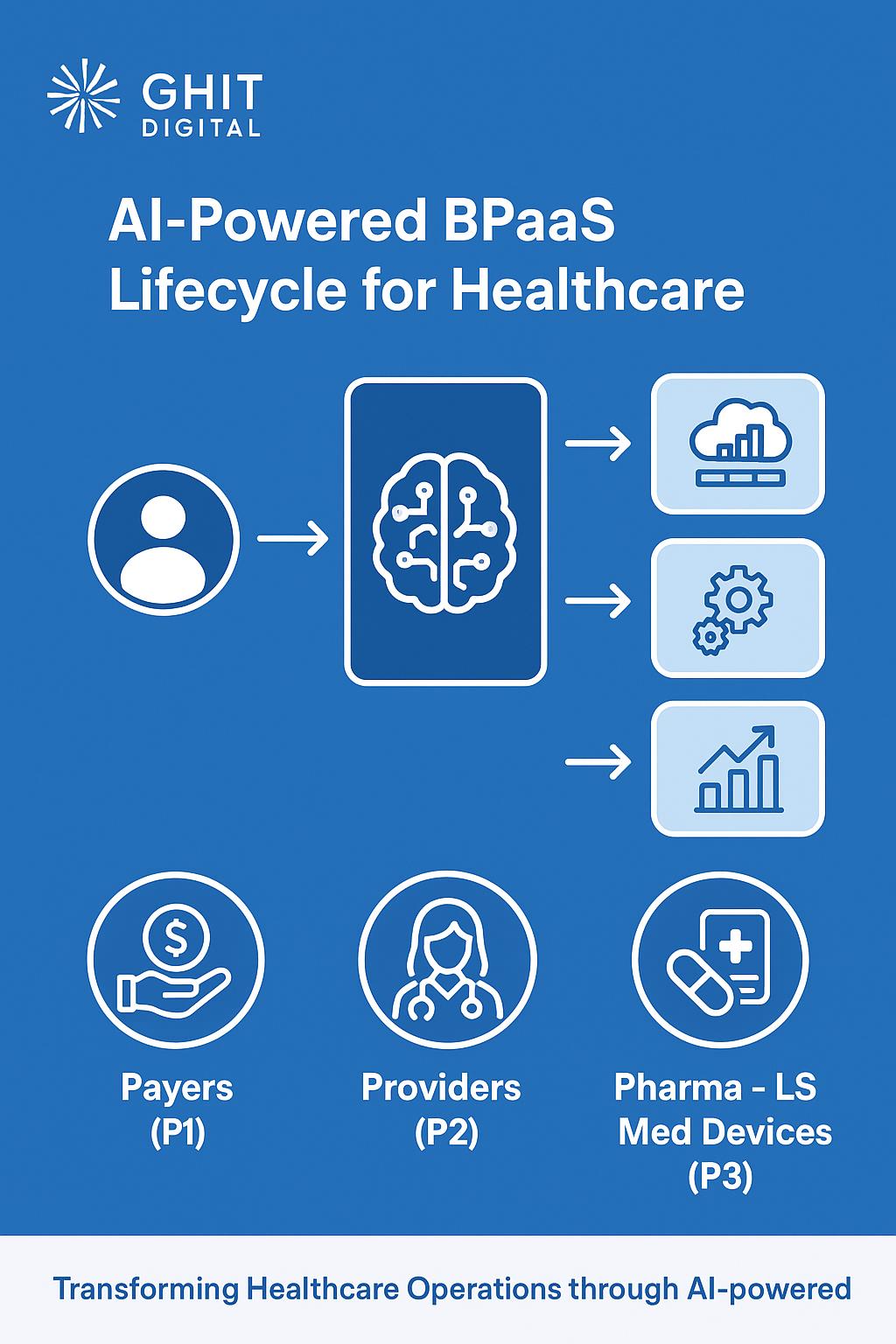

The LTC insurance industry, characterized by its specialized workflows, intricate claims adjudication, and strict regulatory environment, is ripe for digital transformation.4 GHIT Digital, leveraging the NewgenOne platform, offers a comprehensive, AI-powered, low-code solution specifically designed to address these challenges and empower LTC carriers.

NewgenOne is a unified ECM + BPM + CCM solution that can:

Automate policy administration and underwriting with AI-powered decision support, streamlining complex processes and reducing human error.5

Manage claims workflows efficiently with real-time data and document management, leading to faster adjudication and payout.6

Enable personalized communications that significantly improve member engagement and satisfaction.

Offer customizable low-code interfaces for rapid adaptation to evolving regulatory requirements or business changes.

Integrate seamlessly with core systems, Electronic Health Records (EHRs), and external data feeds, creating a holistic view of the policyholder.

This innovative approach translates directly into faster claims processing, enhanced compliance, and a superior customer experience, crucial differentiators in today's competitive LTC insurance market.

To further demystify LTC insurance, here are some critical FAQs and their practical answers:

Q: What certifies eligibility for LTC benefits?

A: The certification by a licensed physician that an individual has a severe cognitive impairment or inability to perform a specified number of Activities of Daily Living (ADLs) is called a benefit trigger.7 This initiates eligibility for benefits under most tax-qualified LTC policies.

Q: How do LTC policies typically trigger benefits related to Activities of Daily Living?

A: Most tax-qualified LTC policies trigger benefits when an individual is impaired in at least two ADLs. This is a standardized federal criterion.

Q: What type of care suits a person who is mentally alert but physically frail?

A: Such an individual best fits Custodial Care, which involves assistance with ADLs but no skilled medical care.8

Q: How does an integrated LTC rider affect the death benefit of a life insurance policy?

A: If a policyholder collects $50,000 in LTC benefits on a $150,000 life insurance policy with an LTC rider, the remaining death benefit is reduced accordingly to $100,000. LTC riders typically accelerate part of the death benefit to cover care costs.9

Q: How do insurers typically respond when an applicant is a substandard risk?

A: They are least likely to give a premium discount. Instead, they may increase the elimination period, reduce benefits, or shorten the benefit period to mitigate risk.10

Q: What type of care does “skilled care” refer to?

A: Care provided by licensed healthcare professionals under medical supervision. This requires clinical expertise, unlike custodial care.11

Q: Who qualifies for Medicaid in the context of LTC?

A: Medicaid eligibility for LTC typically requires meeting strict income and asset limitations, as it is a needs-based program.

Q: Which care plan focuses on comfort rather than cure?

A: The maintenance plan of care addresses chronic conditions with no curative treatment, focusing on comfort, similar to palliative and hospice care principles.

Q: What does the Restoration of Benefits Clause entail?

A: Benefits are restored to original levels once a patient is certified treatment-free for at least six months.12 This prevents depletion of benefits for recoverable periods.

Q: What is the most cost-effective way to keep pace with rising LTC costs?

A: Purchasing an automatic benefit increase option. This inflation protection helps maintain purchasing power over time.

The growing need for long-term care, coupled with the complexities of the current system, demands innovative solutions.13 GHIT Digital, with its deep expertise in digital transformation and healthcare technology, offers the cutting-edge NewgenOne platform to future-proof your LTC business operations. By embracing AI-powered, low-code solutions, LTC carriers can achieve unparalleled efficiency, compliance, and customer satisfaction.14

If your organization is considering issuing an RFP for enterprise software solutions tailored to Long-Term Care insurance, we invite you to connect with Monica Vashishtha, President and COO of GHIT Digital. With over 25 years of expertise, Monica is ready to discuss how GHIT Digital can empower your business.

Ready to explore how our AI powered, advanced LowCode technology platforms can transform your healthcare Payers (P1) & Providers (P2) organization, specific to

A) ECM (Content Management)

B) BPM (Workflows Management)

C) CCM (PHI / HIPAA Communication Management)

D) PLM (Provider Lifecycle Mgt)

E) ANG (Appeals & Grievances Mgt)

F) EHR Connector (FHIR)

G) EHR Archival (EAMS)

We invite you to connect with us for a no-obligation discovery conversation or DEMO

Call us at +1 201.792.8924 or +1 646.734.6482 . Alternatively, email us at Monika@GHIT.digital . We also welcome your RFPs/RPQs for timely review and response.

#GHIT, #GHITDigital, #RFP, #Newgen